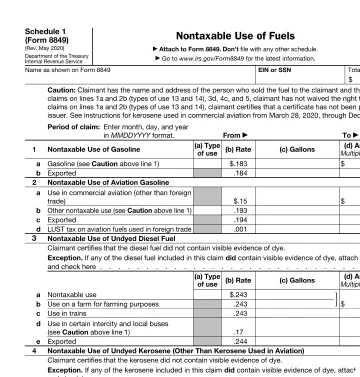

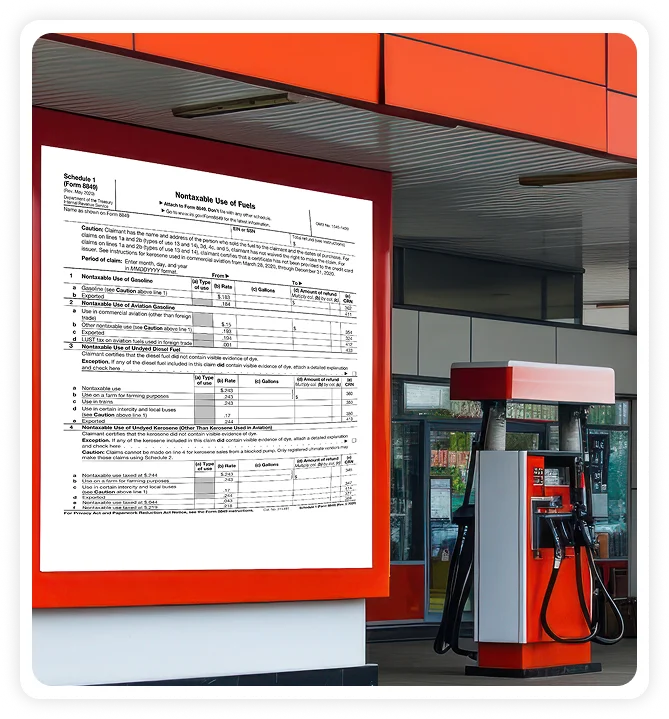

- Schedule 1 is a part of IRS Form 8849, Claim for Refund of Excise Taxes. It is used to claim a refund of federal excise tax paid on fuels that were used for nontaxable purposes.

- This schedule applies when fuel is purchased with federal excise tax included, but is later used in a manner that is not taxable under IRS regulations. Typically, the claim is filed by ultimate purchaser of the fuel.

- Using Form 8849 Schedule 1, a taxpayer can claim a refund of federal excise taxes paid on fuels used. A taxpayer has to file the schedule to not only claim the tax benefits but also to abide by the federal excise tax laws.