Emailsupport@efile720.com

Support (628) 267-4400

(Monday - Friday 5:00 am to 7:00 pm PST)

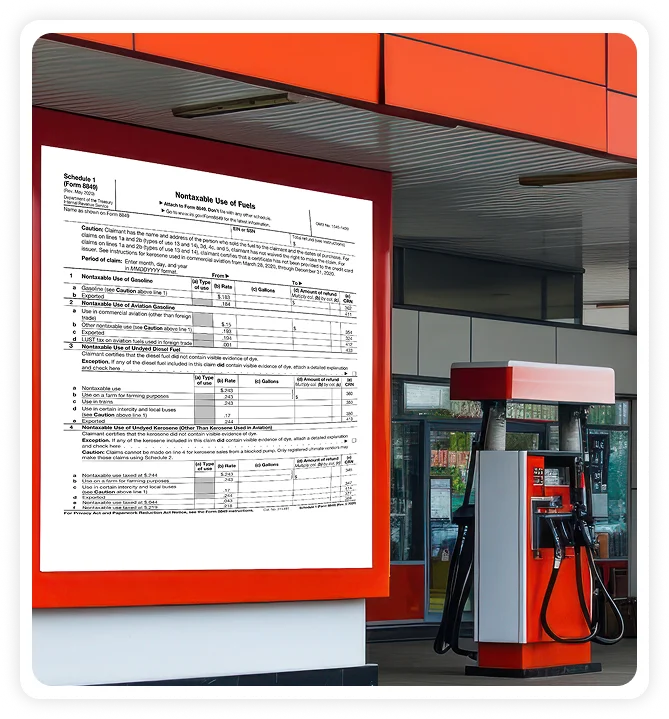

Schedule 8 is filed by IRS-registered credit card issuers (as per Form 637, Registration Type "CC") that had to pay Section 4081 tax on gasoline, diesel, kerosene, or aviation fuel that was sold to nontaxable users and paid through credit card transactions.

The following are eligible filers:

The claimant should prove the tax paid on fuel sold for nontaxable purposes by providing evidence of a credit card payment, so the credit/refund claim can be considered legal.

Schedule 8 specifies the different fuel types and exempt uses for the claims. For each line, input:

The totals from all lines should be transferred to Form 8849, Line 8.

| Line | Fuel Type | Exempt Buyer | Columns: Rate (a), Gallons (b), Tax Paid (f) |

|---|---|---|---|

| 1a | Gasoline | Nonprofit educational org | Enter Here |

| 1b | Gasoline | State/local government | Enter Here |

| 2a | Undyed diesel | State/local government | Enter Here |

| 2b | Undyed kerosene | State/local government | Enter Here |

| 3a | Aviation gasoline | Nonprofit educational org | Enter Here |

| 3b | Aviation gasoline | State/local government | Enter Here |

| 4a | Aviation-grade kerosene | State/local government | Enter Here |

| 4b | Other kerosene | State/local government | Enter Here |

It performs a Form 720 record search for CC transactions and then auto-fills the reg. no., nontaxable dates, fuel type/gallons.

It is guided by the current 4081 rates; it displays the total claim amount before submitting.

It links statements/invoices with specific lines; it provides information about mismatches.

The system perfectly meets IRS CC regulations; quicker refunds to the submitting through the MeF are feasible.

The dashboard tracks acceptance/refund status, days, not months.

| Quarter of Fuel Use | Filing Period | Due Date |

|---|---|---|

| Jan-Mar (Q1) | Apr 1 - Jun 30 | Jun 30 |

| Apr-Jun (Q2) | Jul 1 - Sep 30 | Sep 30 |

| Jul-Sep (Q3) | Oct 1 - Dec 31 | Dec 31 |

| Oct-Dec (Q4) | Jan 1 - Mar 31 | Mar 31 |

With the IRS now constantly emphasizing electronic filing, it is more important than ever to understand e-filing because it is becoming the standard.

Read More

If a company is in the business of providing tanning services to consumers, it must The collected tax must be reported and remitted to the IRS by filing IRS Form 720 on a quarterly basis.

Read More

Owning or operating a tanning salon comes with unique operational and financial responsibilities. One area where many business owners struggle is tax compliance.

Read More