Emailsupport@efile720.com

Support (628) 267-4400

(Monday - Friday 5:00 am to 7:00 pm PST)

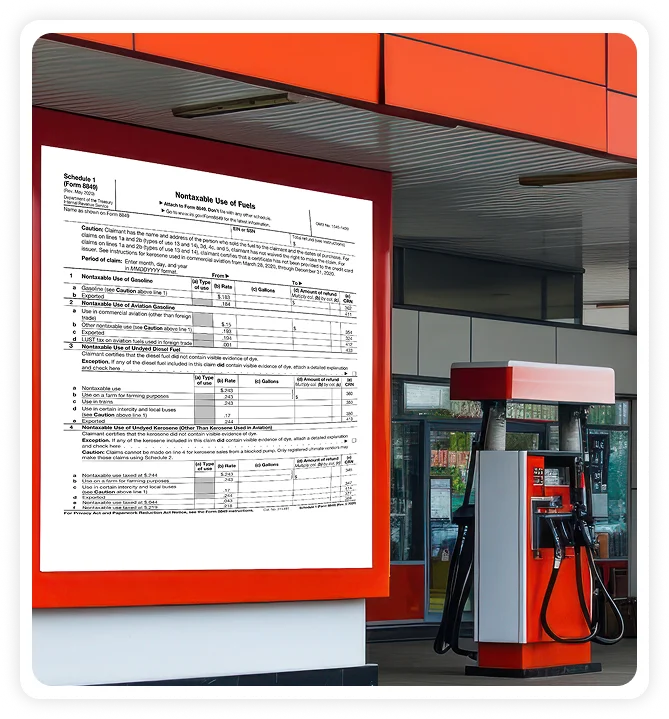

Schedule 6 is the record of those taxpayers who have paid the excise tax in excess via Forms 720, 2290, 730, or 11-C, and their refund request is not covered by any other schedule.

The following are among the taxpayers:

Claimants who request refunds must provide records of the payments made and how they have been overpaid.

Some of the main proof includes:

In line with Schedule 6, one should state the Claim Reference Number (CRN), tax paid, and the refund amount per line (no per-gallon data). The totals after adding up all the schedules and the $750 threshold being applied are carried over to Form 8849.

Schedule 6 is intended to cover a variety of excise overpayments that cannot be matched with other schedules:

Determine Schedule 6 eligibility for Forms 720/2290 claims; automatically couple VIN/mileage to minimize mistakes.

Derive pro-rata from consolidated inputs; correctly applying thresholds.

Drives doc, CRNs, thresholds, and proof criteria.

Status is tracked live; refunds are sped up through a dashboard.

| Quarter of Fuel Use | Filing Period | Due Date |

|---|---|---|

| Jan-Mar (Q1) | Apr 1 - Jun 30 | Jun 30 |

| Apr-Jun (Q2) | Jul 1 - Sep 30 | Sep 30 |

| Jul-Sep (Q3) | Oct 1 - Dec 31 | Dec 31 |

| Oct-Dec (Q4) | Jan 1 - Mar 31 | Mar 31 |

With the IRS now constantly emphasizing electronic filing, it is more important than ever to understand e-filing because it is becoming the standard.

Read More

If a company is in the business of providing tanning services to consumers, it must The collected tax must be reported and remitted to the IRS by filing IRS Form 720 on a quarterly basis.

Read More

Owning or operating a tanning salon comes with unique operational and financial responsibilities. One area where many business owners struggle is tax compliance.

Read More